Primer: An America First Vision for Health-Care

Synopsis

While the United States has some of the highest-quality physicians and care in the world, its health-care bureaucracy is an abject failure. This bureaucracy is dominated by the collusion of weaponized government, corporate cronyists operating in the insurance industry, and the greed of the pharmaceutical lobby. The web formed by these entities has, over time, established a system that increasingly socializes both cost and access to care while maintaining the illusion of a free market.

In truth, the United States has not had a market-based system in health care for generations. Instead, the system is mostly run by government bureaucrats and insurance executives who seize and then redirect taxpayer resources to fund their bureaucracies. And instead of a focus on quality of care and cost, debates often operate on progressive terrain where emphasis is solely on “coverage.” This is a mostly meaningless metric that simply evaluates the number of people who can claim to have a piece of paper assuring providers that some percentage of their services rendered will be either directly subsidized for the patient or reimbursed by the government for the provider.

As Congress debates reviving expired COVID-era federal subsidies,1 the focus of elected officials unfortunately remains on propping up this failed bureaucracy and the bureaucrats responsible for much of the misery inflicted on patients. It is long past time for Congress to undo the damage it has caused and put the American people first. Indeed, this failed progressive health-care machine is at the center of America’s family formation crisis—a crisis marked by a sense that everything from a good home to dependable child care to a quality doctor is priced beyond what hardworking Americans can now afford.

A critical step in resolving this family formation crisis is cutting the Gordian knot of bureaucratized health care. This first requires conservative elected officials to stop trying to salvage America’s harmful, quasi-socialist system out of a feeling of obligation to constituents because of a perceived lack of viable alternatives.

Background: The Cancerous Effect of Obamacare

As political leaders debate “affordability” and Americans continue to suffer from persistent cost increases due to the Biden-era government spending spree, it’s essential to review the role that Obamacare has played and continues to play in exacerbating cost increases and lowering the quality of care.

Arguably, no piece of legislation better captures the cynical and destructive progressive vision for American health care than the Affordable Care Act, better known as Obamacare. Since its passage in 2010 and its implementation in 2013, the law has wreaked havoc on working Americans through skyrocketed premium increases, diminished access to care, and supersized Medicaid enrollment. The legacy of Obamacare is one that directly contributes to out-of-control state budgets and overwhelmed families who now frequently pay more for their monthly health insurance than their mortgage.

Critics at the time warned that Obamacare was structurally designed to fail by entrenching insurer dominance while relying on fragile regulatory assumptions rather than producing a genuinely competitive or sustainable health-care market.2 Unsurprisingly, Obamacare was presented in a much different light. President Barack Obama touted his approach as an effort to cover the uninsured and “bring down premiums by $2,500 for the typical family.”3 Instead, Medicaid expansion to healthy adults accounted for 75 percent of the “newly insured” under Obamacare through the first three years of the law’s implementation,4 millions of Americans were thrown off their existing health insurance plan, and premiums increased by a staggering 169 percent over the last twelve years.5

That’s because the core of the law, its statutory details aside, remains relatively straightforward: onerous one-size-fits-all regulations imposed on insurance policies and massive Medicaid expansion to healthy adults. Progressive proponents who brag about the law reducing the number of uninsured Americans ignore the fact that vast swaths of those numbers came from bribing states into shoving healthy adults onto Medicaid rolls.6

According to the Centers for Medicare and Medicaid Services, the average number of monthly enrollees in Medicaid in 2013 was 57.4 million.7 In 2023, the average number of monthly enrollees in Medicaid was 91.4 million, a 59 percent increase in Medicaid recipients ten years after the implementation of Obamacare.8 That number has slowly dropped to around 77 million enrollees as states have pared back pandemic-era policies that significantly relaxed and expanded Medicaid eligibility criteria. Medicaid has seen at least $1.1 trillion in fraudulent payments since its Obamacare expansion9 and remains a weaponized monstrosity destroying the lives of children through DEI practices and mutilative gender-transition services.10

An estimated 9.3 million Americans lost their existing health insurance coverage when Obamacare was enacted.11 This had devastating effects on households across the nation.

In one particularly alarming case, a sixty-year-old football coach and math teacher in Alabama lost his existing BlueCross BlueShield health insurance plan when Obamacare was implemented on October 1, 2013, and his monthly premium skyrocketed from $405 to $1,380.28.12 Because his employer-provided insurance was now too costly and the Obamacare exchange plans were both expensive and lacking in access to quality physicians, he opted for a sharing association until he qualified for Medicare in 2018. When he was diagnosed with stage 3 colon cancer in 2017, one year before Medicare eligibility, he had to rely on a GoFundMe effort to pay for the cancer treatment needed to save his life.13 The BlueCross BlueShield plan that Obamacare canceled would have covered much of his treatment.

Obamacare also expedited the consolidation of viable health insurers through the imposition of its cost-driving Title I regulations such as Guaranteed Issue, Medical Loss Ratio, and Community Rating. What began as “horizontal merger” attempts in which corporate insurance entities such as Aetna tried to buy Cigna soon transformed into “vertical mergers” wherein health insurers began merging with large pharmaceutical companies and pharmacy benefit managers, effectively creating powerful monopolies that married payers to providers.14

This consolidation spread to hospital systems and provider networks. A 2018 report from The Wall Street Journal revealed that hospital mergers doubled in the years following the passage of Obamacare.15 Roughly 25 percent of doctors were employed by hospital systems in 2012, before the implementation of Obamacare. By 2022, that number skyrocketed to 55 percent.16

The consequences of insurance regulations and Medicaid expansion were predictable even before the passage of the law: less competition, fewer patient-focused doctors, bloated bureaucracies, and skyrocketing costs that intentionally inflict pain on working Americans. That is precisely what occurred.

Impacts: Assessing the Fallout

Even institutions that benefit from the existing paradigm admit the failure of the post-Obamacare system. A study released by Johns Hopkins in 2023 showed that cash prices for roughly 47 percent of hospital services were either lower than or equal to the median insurer price for the same procedure in the same hospital with the same service setting.17 This should not be shocking. Under Obamacare, insurers must cover the costs of the law’s one-size-fits-all Title I regulations. One of those provisions is Guaranteed Issue, a regulation often cited as “protecting preexisting conditions.” However, this mandate requires insurers to provide plans that do not differentiate between healthy individuals and chronically ill individuals with comorbidities, thereby fueling price increases as younger and healthier individuals and families subsidize the indigent and sick.

Couched in terms of protecting the most vulnerable, the real effect of Guaranteed Issue is a supercharged welfare requirement that raises prices on healthy workers to bankroll corporate insurance giants: Contemporary estimates suggest that this one regulation increased premiums by as much as 45 percent.18 The result is that forgoing health insurance entirely and opting for cash payment for medical services is often the more sensible financial option for individuals.

A second reason that self-pay is now often cheaper than insurer-negotiated prices is the massively expanded health-care bureaucracy. From 1975 to 2019, the number of physicians in the United States increased by 200 percent while the number of health-care administrators grew by an eye-popping 831 percent.19 According to the Bureau of Labor Statistics, medical and health service managers were slated to see a 23 percent growth in jobs from 2024 to 203420 compared to just 3 percent for physicians and surgeons.21

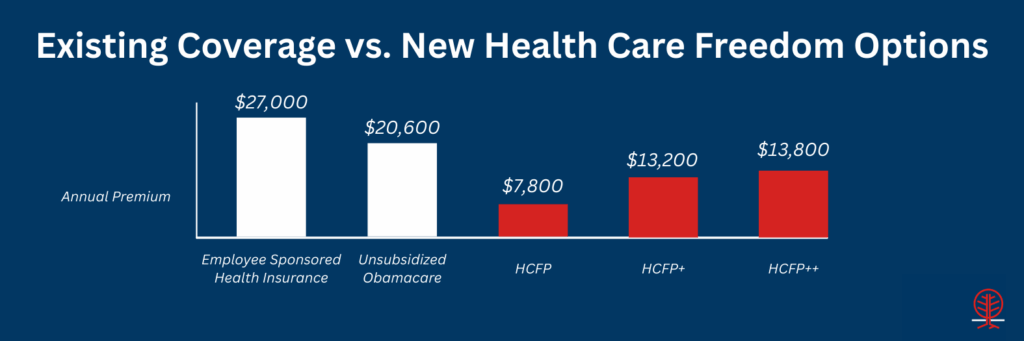

Today, the average annual cost of health care for a family of four with employer-sponsored health insurance is $27,000.22 The average annual cost of an unsubsidized Obamacare Exchange plan for a family of four making $100,000 per year is roughly $20,600, more than 20 percent of the household’s income.23 Even the subsidized Obamacare Exchange plan for this hypothetical family is more than $6,500 on an annual basis.

Obamacare’s subsidy structure perpetuates a massive fraud against Americans. As Congress attempts to strike a desperate bipartisan deal to keep the money flowing to bureaucrats and insurers, it’s important to note that these enhanced subsidies “protect” buyers from the impact of premium increases but ensure that taxpayers pay more when those premiums inevitably rise. The result is loading a perpetual premium increase on the backs of taxpayers—a deliberate theft scheme if there ever was one.24

A Better Way: Health-Care Freedom Puts Americans First

Putting Americans first in public policy approaches is the cornerstone of the agenda for solving the myriad issues facing civil society. Health care is no different: It requires a fundamental paradigm shift in how policymakers think about the delivery of care, the best interests of patients, and the formation of families.

The vast majority of problems in health policy stem from government interference and federal statutes that put bureaucrats between patients and doctors, socialize the cost of care through supercharged welfare programs, emphasize meaningless coverage quotas over quality providers, and funnel Americans into programs that provide the biggest payouts to corporate insurers. These systematic failures are intentional and date back to President Franklin D. Roosevelt’s New Deal, running through President Lyndon Johnson’s catastrophic Great Society and President Obama’s destructive Affordable Care Act.

A better way forward emphasizes health-care freedom through a personalized approach to care with an empowered, civil society–based safety net. In 2024, Representative Chip Roy (R-TX) put forward a proposal, “The Case for Healthcare Freedom,” that laid out many of the provisions found below.25 The America First plan takes inspiration from that thoughtful framework and incorporates additional numerous policy considerations and proposals.

Direct Primary Care

An increasingly popular option for Americans priced out of the Obamacare Exchanges or facing skyrocketing monthly premiums is concierge-based care through a direct primary care (DPC) provider. This model is simple and effective. A primary care physician simply chooses to opt out of the failed government-insurer model that colludes against patients and enriches bureaucrats. Patients typically pay a monthly subscription—akin to a retainer—to the DPC provider in exchange for care. Health insurance is not accepted. Medicaid is not accepted. Doctors interface with patients directly and as often as necessary.

The direct care model is also increasingly being adopted for specialty services. The Surgery Center of Oklahoma famously operates as a direct care institution, accepting cash payment for services at lower prices and with better quality than existing insurance and government programs.26

Paradigm Shift: Congress should build on the One Big Beautiful Bill Act, which finally resolved regulatory confusion on DPC payments by recognizing DPC as a medical expense rather than a form of health insurance. The eligibility of portable health savings accounts (HSAs) should be extended to include all direct care services, including direct specialty care, with explicit language that allows HSAs to be used toward licensed health services that do not include abortion, genital mutilation, or gender-transition procedures. More on HSAs can be found below.

Further, Congress should break the big-insurer monopoly by incentivizing an increased supply of DPC and direct specialty care providers and practices. This is key to putting Americans first over government bureaucrats and crony C-suite executives. Among the provisions needed are the following:

- Reduce interest rates on any subsidized loan taken out for medical school if the graduate is employed by or operates a direct care practice for at least five years.

- Implement a federal income tax exemption for direct care service providers after operating a DPC or direct specialty care practice for more than five years.

Health Savings Accounts

HSAs themselves are not a substitute for fully extracting Americans from the tangled government-insurer web, but promoting them is an integral component of health-care reform that provides a tax-free pool for health expenditures. HSAs help defray cost burdens and put patients in control of expenditures. They are triple tax-advantaged, meaning contributions aren’t taxed, account growth isn’t taxed, and withdrawals for qualified medical expenses aren’t taxed. The One Big Beautiful Bill Act resolved a lingering issue within federal rules by allowing for HSAs to be used for DPC expenditures as of January 1, 2026.

Paradigm Shift: Congress should build on the HSA momentum by removing existing restrictions on who can have an HSA, what they are used for, and how much can be contributed. Lawmakers should consider several approaches to maximize the utility of HSAs. Among the provisions needed are these:

- Permanently remove the linkage between HSAs and high-deductible plans. Tether HSA eligibility to Social Security numbers so that HSAs are essentially accounts owned by citizens that can be used by anyone for any qualified medical expense.

- Eliminate all contribution caps and limits.

- Authorize states to further expand and determine what constitutes a qualified medical expense, with strict prohibitions on abortion services, genital mutilation, and gender-transition procedures.

- Allow crossover funds so that HSAs can be shared between family members and, like 529 savings accounts, beneficiaries can be switched if necessary.

- Expand Health Opportunity Accounts for Medicaid recipients. The Deficit Reduction Act of 2005 (DRA) established these accounts as a pilot program, allowing states to offer HSA-like accounts to Medicaid beneficiaries for out-of-pocket health expenditures.27These accounts should be made available across the Medicaid population for DPC and direct care services. Congress should repeal existing restrictions that limit opportunity account participants to 5 percent of a managed care organization population and just a handful of states, amending the existing DRA language. The advantage of this approach is that instead of reimbursing providers and supercharging the ongoing provider tax scheme that pilfers from taxpayers, this setup eliminates the middleman and pays Medicaid recipients a formula-based amount based on income and health status relative to eligibility status. The closer an individual is to being ineligible for Medicaid coverage, the more the amount that is paid out, up to a maximum of $1,500 per child and $3,000 per adult, for example. This will incentivize healthier habits and encourage employment.

Supercharged Sharing Associations

Health-care-sharing ministries are groups of people who have decided to pool funds for medical expenses that aren’t subject to most state and federal health insurance regulations.28 These entities are better categorized as cost-sharing organizations, and they are often cheaper than traditional insurance. Obamacare provided a select carveout for sharing associations and ministries that have been in operation since before 1999, exempting them from the Title I insurance regulations of the law.

Paradigm Shift: Sharing associations operate at a national level. Lawmakers should give Americans new options to avoid the government-insurer leviathan through these kinds of associations. There is one key provision needed:

- Repeal language in Section 5000 of Obamacare that restricts exemptions for sharing associations operating before 1999, and provide new statutory language that provides for new sharing associations to operate outside the Obamacare regulatory infrastructure.

Infinite Risk Pools

The concept of risk pools received significant attention during the initial debate over Obamacare and the subsequent repeal efforts in 2017–18. However, instead of state-run pools funded by taxpayers to offset health costs for the most indigent, policymakers should take a radical approach that empowers community-driven risk pools. These infinite risk pools, akin to sharing associations, should allow voluntary associations to share resources to defray the costs of qualified medical expenses, with the minimum amount of regulation.

Infinite risk pools allow citizens to form risk pools among their neighbors, family members, friends, churches, synagogues, parents’ organizations, etc. The general structure for how these pools operate is straightforward:

- A group of like-minded individuals bands together and files paperwork with the state with the intention of setting up a risk pool.

- The risk pool must be linked to a licensed financial institution to mitigate fraud and ensure accountability of funds.

- The risk pool operates under the supervision of a manager or a committee of members.

- The risk pool makes a determination on monthly contribution requirements.

- Whenever a medical expense is needed, the pool manager or committee prioritizes which member needs the pool resources (akin to triage) and notifies all members of the expenditure.

Paradigm Shift: Any group of people numbering at least ten individuals should be able to file the requisite paperwork with the state, appoint the pool manager(s), and set the contribution requirements, so long as all recipients receive a monthly account statement and notification of pending expenditures. This approach breaks the big-insurer model and puts patients in control of their care, especially when paired with DPC or direct specialty care. Among the provisions needed to amplify infinite risk pools are the following:

- Statutory changes that preempt states from banning infinite risk pools and incorporate prohibitions for using risk pools for abortion services, genital mutilation, and gender-transition procedures

- Tax-deductible contributions from both individuals and businesses to infinite risk pools if such entities are not members of the specific pool. This provides another avenue for the infinite risk pool to be used to help defray unforeseen medical expenses for those within the pool and provides an incentive for such contributions.

Catastrophic Coverage

Health insurance does not operate like traditional insurance. Obamacare’s preexisting conditions mandates transformed the entire industry into a thinly veiled welfare scheme that makes it illegal for insurers to take health status into account. Undoing this scheme is of paramount importance for reinvigorating a healthy catastrophic coverage market.

Catastrophic plans typically offer very low premiums with high deductibles and cover expensive, unexpected medical expenditures. These plans might not be the best option for someone who prefers a lower deductible, but they may be a good choice for healthier individuals who don’t want to pay higher monthly insurance premiums. Importantly, these plans still protect against the risk of cancer or major surgeries.

Paradigm Shift: Health insurance must once again operate like traditional insurance, focused on mitigating the risk of a house fire or totaled car as opposed to paying for a new light fixture or oil change. Congress should focus on restoring low-cost, big-event catastrophic plans to the market. Among the necessary provisions of this approach are these:

- Repeal the Title I regulations in Obamacare at the federal level, followed by a state opt-in trigger that allows progressive states like California and New York to readopt the Obamacare architecture if they so choose. This is not a full repeal, but rather a reset that defaults to deregulation while giving progressive states the option to “keep their Obamacare if they like Obamacare.”

- Once the Title I regulations have been repealed at the federal level, statutorily eliminate existing restrictions that prohibit catastrophic coverage holders from also having an HSA and that set arbitrary age requirements.

Impacts of an America First Health-Care Freedom System

Together, these overlapping policies provide a personalized approach to care with a strong community-based safety net that would have life-changing results for American families. For example, an average family of four with two forty-five-year-old parents and two children on employer-provided insurance would see the following improvements:

- Enhanced Direct Primary Care: If this family fully switched over, opting out of the existing health insurance system entirely, and instead chose a DPC provider using median DPC prices,29 the savings would be roughly $1,900 per month or $23,000 per year in both premium payments and employer contributions compared to the average employer-provided plan.30 This family would save $1,400 per month or $17,000 per year compared to an unsubsidized Obamacare Exchange plan. Even on a subsidized Exchange plan, average savings from fully switching to a DPC provider would equal roughly $250 per month or $3,000 per year.

- Health Savings Accounts: This family could further defray costs through uncapped and portable HSAs. Now that the One Big Beautiful Bill Act has changed the definition of DPC providers, HSAs can be used for DPC subscriptions. Just 10 percent of the savings from using a DPC provider would provide this family with anywhere from $300 to $1,300 per year for unforeseen medical expenses.

- Supercharged Sharing Associations: This family could also switch over to sharing associations—using the existing entities that already offer plans at half the price of most employer-sponsored and Exchange plans. Repealing the restrictions on new sharing associations would bolster competition, pressure provider systems to accept sharing associations as a form of insurance, and lower costs for members even further.

- Infinite Risk Pools: This family could decide to join together with their church or their neighborhood for a locally run and managed risk pool. If this family attends their 100-member church and chips in a required minimum of $50 per month per member, this family could have access to $60,000 for medical emergencies or unforeseen expenses as a community-based backstop to pay for care.

- Catastrophic Coverage: Lastly, this family could make use of newly-rejuvenated catastrophic coverage insurance plans in case of a chronic disease or cancer diagnosis. These plans on average cost around $3,600 per year or, in the event of having to hit a deductible, $10,600 per year.31

Scenario 1 Result: This family of four decides to replace its single, exceedingly costly employer-provided health insurance plan with a suite of discrete tools to manage the whole family’s health-care needs. The family switches to a DPC provider, contributes a portion of savings to a tax-free HSA, joins a church-run risk pool, and purchases catastrophic coverage. The average estimated total cost for this arrangement is $7,800 per year for higher-quality concierge primary care, access to more than $60,000 in personal and community-based safety nets, and a catastrophic coverage backstop should anyone become seriously ill and require specialty care. This family would also save roughly $19,200 in both monthly premiums and employer-provided contribution costs per year.32

For a similar family of four on an unsubsidized Exchange plan that chooses a similar path to use a DPC provider, chip in savings for an HSA, join a 100-member risk pool, and pay for catastrophic coverage, the savings would be roughly $12,800 per year in premiums. For a family on subsidized Exchange plans that chooses an identical path, the cost would be an estimated $1,200 more per year. However, this may be a price worth paying given the access it gives to higher-quality and personalized care, control over dollars, and access to community-based pools to defray the modest cost increase.

Scenario 2 Result: Instead of joining an infinite risk pool, this family of four opts to join a health-sharing ministry.33 Similar to the first scenario, the family also accesses a DPC provider, makes use of tax-free HSAs, and pays for newly reconstituted catastrophic coverage provisions. The estimated cost for this arrangement is $13,200 per year. This still results in significant savings compared to employer-provided coverage—around $13,800 in monthly premiums and employer contribution costs per year.34 If the family uses this approach instead of unsubsidized Exchange plans, the savings would be an estimated $7,400 per year in premiums. For a family on subsidized Exchange plans that chooses an identical path, the cost would be significantly more, at roughly $6,600 per year.

Scenario 3 Result: This family of four chooses to use the entire suite of available options to fully mitigate risks. The estimated cost for this arrangement (wherein the infinite risk pool is a 100-member church with $50 monthly contribution requirements) would be $13,800 per year. If the family has employer-provided coverage, savings come out to $13,200 in monthly premiums and employer contribution costs. Using unsubsidized plans, the savings would be an estimated $6,800 per year in premiums. For a family on subsidized Exchange plans, the cost would be roughly $7,200 more per year.

An important consideration is that DPC arrangements often lead to significant savings on an annual basis for prescription medications. This is frequently attributed to specific arrangements that DPC providers have with wholesalers for generics and other direct-to-patient services, bypassing pharmacies’ built-in handling costs and operations-based markups. For this family of four, the savings from not having Obamacare-distorted health insurance would likely be in the hundreds of dollars on an annual basis for medications.35

Further, it should be noted that as healthier populations leave the Exchanges, costs will likely increase for subsidized Obamacare plans because those populations are artificially keeping prices down. Contrary to predictable progressive caterwauling, this means that eventually, possibly even relatively soon, the America First health-care freedom approach will become more viable for all populations, including sicker and poorer groups on subsidized Obamacare plans. As those out-of-pocket premiums increase, so too will the savings that come from DPC, HSAs, sharing associations, infinite risk pools, and catastrophic coverage backstops.

For example, if the average subsidized Obamacare exchange plan for this family of four increases to just $660 per month from its current baseline of $545 per month, the adoption of the America First provisions outlined above would immediately result in savings—on top of better care and access to emergency health expenditure pools.

Additionally, other provisions would create a dynamic environment as direct specialty care operations expand and lower costs, new DPC providers open up practices to create competition for lower prices and better care, and families are protected from the corporate-federal health-care leviathan bankrupting their households.

Nevertheless, in the interim, lawmakers should consider temporarily diverting tariff funding to stabilize the Exchanges as healthier populations exit. This is because costs will likely increase for the subsidized Exchange market as younger and healthier individuals and families exit to receive better care without going bankrupt. The total amount of tariff funding should not fully offset the predictable rise in premiums for those on subsidized Exchange plans but rather provide a buffer as the transition away from Obamacare takes places. Initial funding could be set at $30 billion annually and then slowly taper down to zero over a ten-year sunset.

Tools for Prenatal and Maternity Care

The costs of childbirth can seem too high to afford without health insurance coverage. Thus, the allure of the current Obamacare insurance regime, despite its exorbitant costs and limited provider networks, remains attractive to millions of Americans who fear what would happen without their insurance plan. Under the paradigm-shifting America First framework, new and expanded tools would provide peace of mind in prenatal and maternity care. Specifically, this framework does the following:

- Offers DPC providers who, aside from significantly cheaper monthly costs relative to current insurance options, also frequently have access to cheaper prescriptions if the mother becomes sick during pregnancy

- Offers more standalone birthing centers because of the increased supply of DPC providers, which will partner with these centers and thus lower the costs of childbirth, postpartum care, and facility stays

- Offers expanded and portable tax-free HSAs, which can be shared between family members or designated to new beneficiaries without penalty. This means that parents can deposit funds into an HSA for years (akin to a 529 savings account) so that when their son or daughter is about to have a child, they can use the HSA to pay for the hospital and delivery costs directly through the HSA. Importantly, cash payments for childbirth are often cheaper than insurance.36

- Offers a sharing association option that will negotiate directly with the hospital system using a national risk pool to mitigate total costs37

- Offers an infinite risk pool, which can be used to access community-driven safety net funds to pay for hospital and delivery costs directly. Importantly, these funds are partially contributed by the family having the child, meaning most pools will consider childbirth a priority medical event, triggering payment.

- Offers catastrophic coverage, which can be used in the event of complications during childbirth

Tools for Specialty Care

The fear of not being able to afford treatment for a cancer diagnosis or chronic disease management is the most cited rationale for remaining in today’s Obamacare-fueled health insurance regime. This concern is understandable and in many respects can be a responsible decision to take care of one’s family. However, this cycle can and will be broken with the America First health-care freedom framework. Here’s how:

- DPC providers already offer significant savings compared to current insurance options, and those savings can be deposited into HSAs or infinite risk pools to reduce costs for future chronic or acute medical expenses.38

- As the supply of DPC providers increases, so will the supply of direct specialty care providers. This is because more doctors outside the megamerger hospital systems means more opportunities for arrangements between DPC practices without the need for administrators to sift through insurance paperwork. In other words, direct specialty care leads to both lower costs for patients and more profit for doctors.

- Similar to the above scenario regarding HSAs for prenatal and childbirth expenses, expanded and portable tax-free HSAs can be shared between family members or designated to new beneficiaries without penalty, opening up access to emergency funds. This means that parents, siblings, or aunts and uncles can deposit funds into an HSA for years (akin to a 529 savings account) to help in case of a serious diagnosis.

- Sharing associations directly negotiate with specialty care providers and any hospital systems they are attached to, reducing costs for the patient.

- An infinite risk pool can be used to access community-driven safety net funds to pay for hospital and ongoing care costs directly. Importantly, these funds are partially contributed by the family and individual, meaning most pools will consider a serious health diagnosis a priority medical event and the purpose of the pool, triggering payment.

- Catastrophic coverage provides the ultimate safety net for such an event. In fact, it is the very reason such coverage should be available.

This safety net is far broader, far more flexible, and far more affordable than the existing Obamacare system. Instilling fear of not having insurance is the last weapon that the political left has in its arsenal. That weapon is bankrupting families, delivering worse care, and enriching bureaucrats at the expense of every American. It must and will end.

This America First approach to health-care policy also begins to solve the family formation crisis afflicting young and working-class Americans. When combined with forthcoming proposals on child care, housing, and food from the Center for Renewing America’s Family and Future Initiative, the results will renew America by expanding health-care opportunities that lead to a healthier society.

Conclusion

Nowhere is the impact of government failure felt more than in the health-care sector. Decades of heavy-handed mandates, regulations, and supercharged welfare schemes—alongside crony arrangements that have empowered corporate insurers and large hospital systems—have pushed working-class Americans to the breaking point. The way out is an America First vision that circumvents this system by offering solutions based on a framework of health-care freedom while providing a remedy for our nation’s family formation crisis.

America’s quasi-socialist health-care system drains the fruits of citizens’ labor, transfers wealth from workers to bureaucrats, diminishes individuals’ overall quality of care, accelerates megamergers, and significantly contributes to declining birth rates and delayed marriages. Instead of endlessly debating subsidies designed to prop up the very system harming their constituents, members of Congress should embrace the opportunity to free Americans from the big government–big corporate alliance profiting from our pain.

Endnotes

1. Carney, J. (January 7, 2026). “Senate Group Nears Deal to Revive Obamacare Subsidies,” Politico. https://www.politico.com/live-updates/2026/01/07/congress/senate-deal-obamacare-subsidies-00714048

2. Scott P. Richert, “The Triumph of the Insurance Companies,” Chronicles Magazine, March 22, 2010 (posted June 20, 2022), https://chroniclesmagazine.org/news/the-triumph-of-the-insurance-companies/.

3. Sack, K. (July 23, 2008). “Health Plan from Obama Spurs Debate,” The New York Times. https://www.nytimes.com/2008/07/23/us/23health.html

4. Kominiski, G., Nonzee, N., and Sorensen, A. (December 15, 2016). “The Affordable Care Act’s Impacts on Access to Insurance and Health Care for Low-Income Populations,” Annual Review of Public Health. https://pmc.ncbi.nlm.nih.gov/articles/PMC5886019/

5. Roy, A. (November 13, 2025). “How Much Have Obamacare Premiums and Deductibles Increased?,” Forbes. https://www.forbes.com/sites/theapothecary/2025/11/12/how-much-have-obamacare-premiums–deductibles-increased/

6. Blase, B., Badger, D., and Turner, G. (March 2020). “Affordable Care Act at Ten: Huge Expansion of Welfare and Injury to Individual Insurance Market,” Galen Institute. https://galen.org/assets/ACA_at_10_huge_expansion_of_welfare.pdf

7. HHS Report (2014). “2013 CMS Statistics,” Department of Health and Human Services. https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and-reports/cms-statistics-reference-booklet/downloads/cms_stats_2013_final.pdf

8. Enrollment Data (January 5, 2026). “Medicaid Enrollment and Unwinding Tracker,” Kaiser Family Foundation. https://www.kff.org/medicaid/medicaid-enrollment-and-unwinding-tracker/

9. Greszler, R. (March 18, 2025). “Saving Medicaid by Cracking Down on Misuse and Abuse,” Economic Policy Innovation Center. https://epicforamerica.org/social-programs/saving-medicaid-by-cracking-down-on-misuse-and-abuse/

10. CRA Staff (May 7, 2025). “Primer: The Medicaid Machine Is Destroying Lives As It Devours Budgets,” Center for Renewing America. https://americarenewing.com/issues/primer-the-medicaid-machine-is-destroying-lives-as-it-devours-budgets/

11. Conover, C. (October 31, 2016). “Obamacare’s Five Biggest Broken Promises: Part 1,” Forbes. https://www.forbes.com/sites/theapothecary/2016/10/31/obamacares-five-biggest-broken-promises-part-1/

12. Congressman Mike Johnson (October 22, 2019). “The Conservative Playbook for a Republican Led Congress,” Republican Study Committee, 37. https://mikejohnson.house.gov/uploadedfiles/conservative_playbook.pdf

13. Ibid.

14. Stoller, M. (January 29, 2024). “Obamacare Created Big Medicine,” The Lever. https://www.levernews.com/how-obamacare-created-big-medicine/

15. Matthews, A. (September 18, 2018). “Behind Your Rising Health-Care Bills: Secret Hospital Deals That Squelch Competition,” The Wall Street Journal. https://www.wsj.com/articles/behind-your-rising-health-care-bills-secret-hospinflictital-deals-that-squelch-competition-1537281963

16. Avalere Health Report (April 2024). “Updated Report: Hospital and Corporate Acquisition of Physician Practices and Physician Employment 2019-2023,” Physicians Advocacy Institute. https://www.physiciansadvocacyinstitute.org/Portals/0/assets/docs/PAI-Research/PAI-Avalere%20Physician%20Employment%20Trends%20Study%202019-2023%20Final.pdf?ver=uGHF46u1GSeZgYXMKFyYvw%3d%3d

17. Press Release (April 5, 2023). “Study Finds Hospitals’ Cash Prices for Uninsured Often Lower Than Insurer-Negotiated Prices,” Bloomberg School of Public Health. https://publichealth.jhu.edu/2023/study-finds-hospitals-cash-prices-for-uninsured-often-lower-than-insurer-negotiated-prices

18. White, D. (June 2017). “Unity Through Federalism: Repealing Obamacare’s Regulations and Providing an Opt-In for the States,” Texas Public Policy Foundation. https://www.texaspolicy.com/wp-content/uploads/2018/08/2017-6-PP-UnityThroughFederalismOptInAnalysisWEB-CTAA-White.pdf

19. Drum, K. (June 15, 2019). “Join Me on a Dive down the Rabbit Hole of Health Care Admin Costs,” Mother Jones. https://www.motherjones.com/kevin-drum/2019/06/join-me-on-a-dive-down-the-rabbit-hole-of-health-care-admin-costs/

20. Occupational Outlook Handbook (2024). “Medical and Health Service Managers,” Bureau of Labor Statistics. https://www.bls.gov/ooh/management/medical-and-health-services-managers.htm

21. Occupational Outlook Handbook (2024). “Physicians and Surgeons,” Bureau of Labor Statistics. https://www.bls.gov/ooh/healthcare/physicians-and-surgeons.htm

22. News Release (October 22, 2025). “Annual Family Premiums for Employer Coverage Rise 6 Percent in 2025, Nearing $27,000, with Workers Paying $6,850 Toward Premiums out of Their Paychecks,” Kaiser Family Foundation. https://www.kff.org/health-costs/annual-family-premiums-for-employer-coverage-rise-6-in-2025-nearing-27000-with-workers-paying-6850-toward-premiums-out-of-their-paychecks/

23. Health Insurance Marketplace Calculator (Accessed January 6, 2026). “Four Person Household with $100,000 Income,” Kaiser Family Foundation. https://www.kff.org/interactive/subsidy-calculator/

24. Testimony by Chris Jacobs (December 10, 2025). “Lowering the Cost of Health Care: Technology’s Role in Driving Affordability,” House Oversight Subcommittee Hearing. https://oversight.house.gov/wp-content/uploads/2025/12/Jacobs-Written-Testimony.pdf

25. Representative Chip Roy (2024). “The Case for Healthcare Freedom,” United States House of Representatives. https://roy.house.gov/sites/evo-subsites/roy.house.gov/files/evo-media-document/THE%20CASE%20FOR%20HEALTHCARE%20FREEDOM%20-%20FINAL%20DIGITAL-compressed.pdf

26. Surgery Center of Oklahoma (Accessed January 7, 2026). “Surgery Prices.” https://surgerycenterok.com/surgery-prices/

27. CMS Fact Sheet (November 5, 2007). “Important Facts for State Policymakers: Deficit Reduction Act,” Centers for Medicare and Medicaid Services. https://www.cms.gov/Regulations-and-Guidance/Legislation/DeficitReductionAct/Downloads/Health-Opportunity-Accounts-Backgrounder.pdf

28. Glossary (Accessed January 8, 2026). “What Is a Health Care Sharing Ministry?,” healthinsurance.org. https://www.healthinsurance.org/glossary/health-care-sharing-ministry/

29. Quick Tips Blog (Accessed January 5, 2026). “Answers to Six Common Questions About Direct Primary Care,” American Academy of Family Physicians. https://www.aafp.org/pubs/fpm/blogs/inpractice/entry/dpc-faqs.html#:~:text=3.,of%20two%20low%2Dincome%20patients.

30. Savings for employer-sponsored plans are for both the family and the employer, based on the average monthly premium and average employer contribution made for a family of four. Since employers pay roughly 75 percent of the cost of these plans, employees would have options for a significant increase in take-home pay or enhanced employer payment into an HSA, taken directly from the savings to the employer from not having to pay into the employer-sponsored insurance plan.

31. Insurance Quotes (August 19, 2025). “What Is Catastrophic Health Insurance?,” insurance.com. https://www.insurance.com/health-insurance/coverage/pros-and-cons-of-catastrophic-health-insurance.aspx#

32. See note 29.

33. Average costs for a health-sharing ministry plan for a family of four vary widely among the four primary sharing ministries. The above number is taken from aggregating the monthly averages for a basic/silver-style plan in each of these associations, which comes out to roughly $501 per month.

34. See note 29.

35. SOA Report (May 2020). “Direct Primary Care: Evaluating a New Model of Delivery and Financing,” Society of Actuaries. https://www.soa.org/globalassets/assets/files/resources/research-report/2020/direct-primary-care-eval-model.pdf

36. Berryman, M. (February 5, 2025). “How to Pay for Pregnancy and Childbirth Expenses,” HSA for America. https://hsaforamerica.com/blog/pay-for-pregnancy-and-childbirth-expenses/

37. Costs associated with sharing ministry coverage plans are comparable to existing out-of-pocket costs in the current system. In combination with the other tools outlined here, the cost of delivery and hospital stays will likely be lower than under existing coverage options, and payment options will be significantly more flexible.

38. As mentioned above, these savings included employer-provided contributions, which would translate into increased take-home pay, direct HSA contributions, or a combination of both.

Related Posts

Primer: The Citizenship Act of 2026 and Ending Birthright Citizenship

The left has normalized large-scale unlawful migration; now the Court has detached citizenship from the concept of political allegiance. Without the Citizenship Act of 2026, membership in our constitutional community may remain a function of geography rather than law, consent, and reciprocal obligation.